Deciding whether to rent vs buy a home has become one of the most important financial choices in 2026. Rising property prices, changing interest rates, and evolving lifestyle preferences have made the rent vs buy debate more relevant than ever. While homeownership offers long-term asset creation and a sense of stability, renting provides flexibility, lower upfront costs, and freedom from maintenance responsibilities.

The right choice depends on several factors, including your income, financial goals, location, and how long you plan to stay in a property. In many cities, renting may be more affordable in the short term, whereas buying can generate wealth through property appreciation over time. Understanding the true costs and benefits of renting vs buying a home is essential before making a decision.

This guide compares rent vs buy in 2026 to help you determine which option can save you more money, align with your lifestyle, and support your long-term financial goals.

Table of Contents

Key Takeaways

Looking for a quick summary? Here’s the key takeaway.

- In the Rent vs Buy in 2026 debate, renting often makes more financial sense for people who value flexibility and shorter ownership timelines.

- Buying a home may create more long-term value if you plan to stay in one place and manage ownership costs effectively.

- Higher mortgage interest rates in 2026 continue to impact housing affordability and monthly payments.

- Homeownership does not automatically guarantee wealth creation – market conditions and total costs matter.

- Opportunity cost, investment returns, and lifestyle goals can influence whether renting or buying is the better financial decision.

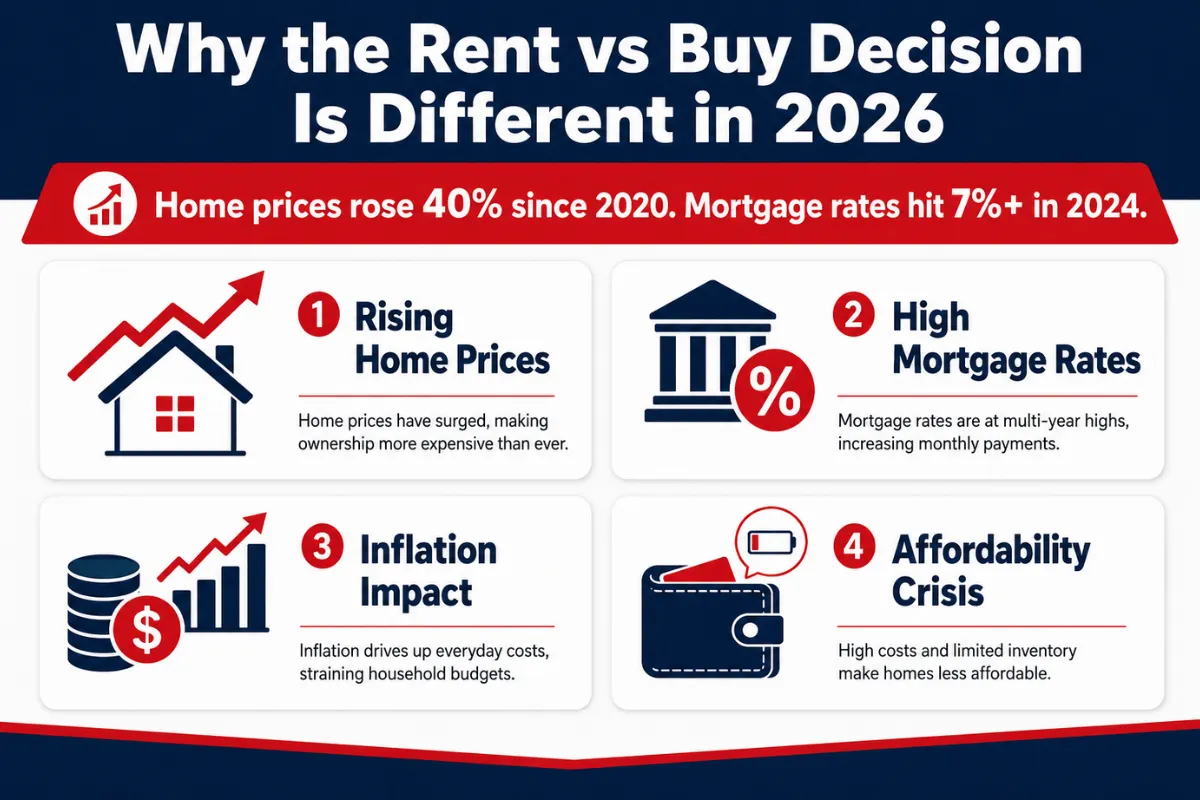

Why the Rent vs Buy Decision Is Different in 2026

Higher Borrowing Costs Changed the Equation

The rent-versus-buy debate looks very different in 2026 because mortgage rates remain significantly higher than the ultra-low levels seen a few years ago. Higher borrowing costs have increased monthly home loan payments, making homeownership more expensive even when property prices remain stable. Buyers now need larger budgets to qualify for mortgages, while the total interest paid over the life of a loan has become a major consideration. As a result, many households are reassessing whether purchasing a home provides enough financial value compared to renting and investing the extra money elsewhere.

Affordability Is Now the Main Decision Driver

Affordability has become the primary factor influencing housing decisions in 2026. Instead of viewing homeownership as the automatic next step, consumers are carefully comparing monthly rent payments with mortgage costs, property taxes, insurance, maintenance expenses, and upfront down payments. In many markets, renting offers greater financial flexibility and lower short-term costs, especially for individuals who may relocate within a few years. However, buying can still be advantageous for those planning to stay long-term and build equity over time. Ultimately, the decision is less about tradition and more about personal financial circumstances, cash flow, housing goals, and local market conditions.

What Are the True Costs of Renting a Home?

Monthly Rent Beyond the Advertised Number

The monthly rent listed in a property advertisement is rarely the complete cost of renting a home. Tenants often face additional expenses that can significantly increase their actual housing budget. These may include utility bills, internet services, parking fees, maintenance charges, renter’s insurance, security deposits, and annual rent increases. In some apartment communities, amenities such as gyms, clubhouses, or security services may also come with separate fees. Understanding these costs is essential when comparing renting with homeownership, as the advertised rent may not accurately reflect the true monthly financial commitment.

Cost Breakdown:

- Base monthly rent

- Electricity, water, and gas bills

- Internet and cable services

- Parking or storage fees

- Renter’s insurance premiums

- Move-in and security deposit costs

- Potential annual rent increases

Flexibility and Financial Mobility

One of the strongest advantages of renting is the flexibility it provides. Renters can relocate more easily for career opportunities, education, or lifestyle changes without the complexities of selling a property. Renting also requires less upfront capital, allowing individuals to preserve cash for investments, emergency funds, business ventures, or other financial goals. This increased liquidity can be especially valuable during periods of economic uncertainty or when interest rates are high.

Cost Breakdown:

- Lower upfront costs compared to a home purchase

- No property taxes or homeowner association fees

- Lower risk of major repair expenses

- Reduced transaction costs when relocating

- Greater access to savings and investment opportunities

While renting may not build home equity, it offers financial mobility and adaptability that can make it a practical and cost-effective choice for many households, particularly those prioritizing flexibility over long-term property ownership.

What Are the Real Costs of Buying a Home?

Many buyers assume that once they can afford a mortgage payment, they can afford a home. In reality, homeownership involves a much broader financial commitment. A mortgage is only one component of the total cost. From upfront expenses to ongoing maintenance and unexpected repairs, understanding the full picture is essential before making a purchase decision.

The Initial Financial Commitment

Before moving into a new home, buyers must prepare for several one-time expenses that can significantly increase the amount of cash needed at closing. These costs often catch first-time buyers by surprise because they are separate from the home’s purchase price.

Common upfront expenses include:

- Down payment

- Closing costs

- Registration and documentation fees

- Legal and attorney charges

- Home inspection fees

- Interior setup and furnishing costs

- Moving expenses

Depending on the property value and location, these costs can add thousands of dollars to the overall investment.

The Ongoing Cost of Homeownership

Once the purchase is complete, homeowners face recurring expenses that continue throughout the life of the property. While mortgage payments are usually the largest monthly expense, they are far from the only one.

Typical costs associated with homeownership include:

- Mortgage principal payments

- Interest charges

- Property taxes

- Homeowners insurance

- Routine maintenance

- Emergency repairs

- HOA costs, if your property is part of an association

- Utilities and service charges

These expenses should be included in any affordability calculation to avoid financial strain.

The Costs Most Buyers Overlook

One of the biggest affordability mistakes is focusing solely on the mortgage payment while ignoring the long-term carrying the long-term costs of homeownership. Maintenance requirements, rising insurance premiums, and unexpected repairs can quickly increase annual housing expenses.

| Expense Category | Financial Impact |

|---|---|

| Down Payment | High upfront cost |

| Closing Costs | Typically 2–5% of purchase price |

| Property Tax | Ongoing annual expense |

| Insurance | Varies by location and coverage |

| Maintenance | Approximately 1–2% of home value annually |

| Repairs | Unpredictable and potentially costly |

Rent vs Buy Cost Comparison for 2026

Comparing the total cost of renting and buying in 2026 helps you understand which option delivers better financial value over time. Explore this 2 BHK rental cost guide to evaluate current rental expenses and compare them with the long-term costs of homeownership.

Example Scenario

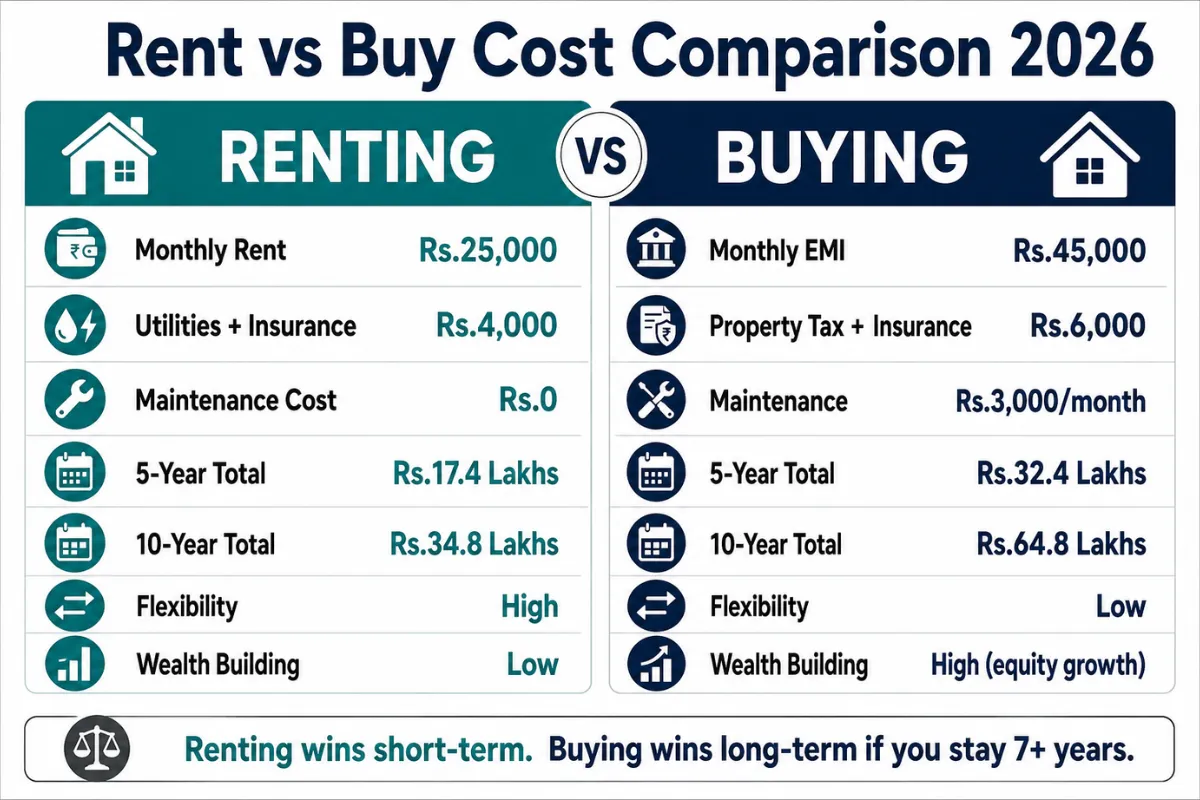

To understand the financial difference between renting and buying in 2026, consider the following example:

- Monthly Rent: ₹25,000

- Home Value: ₹75 Lakh

- Home Loan Interest Rate: 8.25%

- Ownership Period: 5 Years

While actual costs vary by location and property type, this scenario reflects the situation many households face in today’s housing market.

Five-Year Comparison

Both housing options come with pros and cons. Renting typically requires less money upfront and offers greater flexibility, while buying provides the opportunity to build equity and benefit from potential increases in home equity

| Category | Rent | Buy |

|---|---|---|

| Monthly Cost | Lower | Higher |

| Upfront Cash | Low | High |

| Equity | None | Builds Over Time |

| Flexibility | High | Low |

| Maintenance Responsibility | Limited | Full Responsibility |

| Long-Term Potential | Moderate | Higher |

In many markets, renters continue to pay less each month than homeowners. Mortgage payments, property taxes, insurance, maintenance, and repair costs often make ownership more expensive in the short term. However, homeowners gradually build equity through mortgage principal payments, creating a long-term financial asset.

Break-Even Analysis

more cost-effective than renting. In 2026, this timeline has increased in many regions because of higher interest rates and larger upfront costs.

Short stay? Renting often wins because it minimizes upfront expenses and provides flexibility.

Long stay? Buying usually becomes more attractive as equity accumulates and ownership costs are spread over a longer period.

Ultimately, the best choice depends on how long you plan to stay, your financial stability, and whether your priority is flexibility or long-term wealth building.

How Interest Rates Affect the Rent vs Buy Decision

Interest rates are one of the biggest factors influencing the rent vs buy decision. When mortgage rates are low, borrowing becomes more affordable, making homeownership attractive for many buyers. However, higher interest rates increase monthly mortgage payments and the total cost of a home loan, which can make renting a more cost-effective option.

For example, consider a ₹50 lakh home loan with a 20-year tenure. Even a small increase in interest rates can significantly raise your monthly EMI and overall repayment amount.

| Mortgage Amount | Interest Rate | Monthly EMI |

|---|---|---|

| ₹50 lakh | 7% | Example |

| ₹50 lakh | 8% | Example |

| ₹50 lakh | 9% | Example |

As the table shows, a 2% increase in interest rates can add more than ₹6,000 to the monthly payment. Over the life of the loan, this difference can amount to several lakhs of rupees. If comparable rent is substantially lower than the EMI, renting and investing the savings may provide better financial outcomes.

Ultimately, the impact of interest rates depends on your financial situation, local housing market, and long-term plans. Before buying, compare current mortgage rates, expected home appreciation, and rental costs to determine which option offers the best value in 2026.

Opportunity Cost: Should You Invest Instead of Buying?

What Is Opportunity Cost?

Opportunity cost refers to the potential benefits you give up when choosing one option over another. In the rent vs buy debate, buying a home requires a significant upfront investment, including the down payment, closing costs and recurring maintenance expenses. That money could otherwise be invested in assets that may generate returns over time.

Investing vs Building Home Equity

For example, if you invest ₹20 lakh instead of using it as a down payment, the money could grow substantially through compound returns over the long term. On the other hand, homeowners build equity as they pay down their mortgage and may benefit from property appreciation. The better choice depends on factors such as investment performance, local housing market trends, and how long you plan to stay in the property.

Which Option Makes More Financial Sense?

Investing may be more attractive when home prices and mortgage rates are high or when you expect to have short-term housing plans Buying can be advantageous if you plan to stay long term and want the stability and equity-building benefits of homeownership. Before making a decision, compare the potential returns from investing with the expected financial gains from owning a home. Evaluating both scenarios can help determine which option is more likely to grow your wealth over time.

When Is Renting Better Than Buying?

Renting can be a better choice when flexibility, lower upfront costs, and reduced maintenance responsibilities matter more than long-term ownership. Before making a decision, review these essential tenant tips before renting to understand costs, agreements, and factors that can help you choose the right home.

Career and Lifestyle Flexibility

Renting is often the better choice for people who expect major life or career changes. If you may relocate for work, education, or personal reasons within a few years, renting provides the freedom to move without the costs and complexities of selling a property.

Financial Uncertainty and Cash Flow

When income is changing or financial priorities are evolving, renting can reduce financial pressure. Lower upfront costs help preserve savings, maintain emergency funds, and improve monthly cash flow. This flexibility can be especially valuable during economic uncertainty or career transitions.

High Housing Costs and Investment Opportunities

In markets where property prices and mortgage rates are elevated, renting may be more affordable than buying. Instead of committing a large down payment and higher monthly ownership costs, renters can direct surplus funds toward investments, retirement planning, or other financial goals.

Many housing market studies show that renting currently offers stronger monthly cash flow than ownership in several expensive urban areas. While homeownership remains a long-term wealth-building strategy, renting can be the smarter financial decision when flexibility, liquidity, and affordability are the primary priorities.

Renting is not a financial compromise – it is a strategic choice that can align with your lifestyle, career plans, and investment objectives.

When Is Buying Better Than Renting?

Situations Where Buying Wins

Buying a home often becomes the stronger financial choice when you have long-term plans and the financial stability to handle ownership costs. The longer you stay in a property, the more time you have to recover upfront expenses and build equity.

Buying is typically attractive when:

- You plan to stay in the home for 7–10 years or more

- You have sufficient emergency savings

- Monthly mortgage payments fit comfortably within your budget

- Local property values support long-term appreciation

- You want greater housing stability and control

Long-Term Wealth Creation

One of the biggest advantages of homeownership is the ability to build wealth over time. As you repay your mortgage, your equity grows, and any increase in property value can further strengthen your financial position.

Key benefits include:

- Equity accumulation through mortgage payments

- Potential gains from property appreciation

- Protection against rising rental costs

- Long-term asset ownership

Stability Beyond Numbers

Homeownership offers more than financial benefits. It provides stability, predictability, and a sense of permanence that many renters seek.

Owning creates stability – and that stability often has value beyond spreadsheets and financial calculations.

Rent vs Buy Examples at Different Income Levels

The right choice between renting and buying can vary based on income, monthly expenses, and long-term financial goals. Use this 1 BHK rent comparison to understand how housing costs differ across income levels and determine which option offers better value for your situation.

Example Scenarios by Income Level

| Income Level | Monthly Income | Better Choice | Reason |

|---|---|---|---|

| Single Professional | ₹50,000 | Rent | Greater flexibility |

| Middle-Income Family | ₹1,20,000 | Buy | Long-term stability |

| High-Income Buyer | ₹3,00,000+ | Buy | Easier affordability and wealth building |

A single professional earning around ₹50,000 per month may benefit more from renting. Career opportunities, job changes, and relocation needs can make flexibility valuable. Renting also avoids the large upfront costs associated with purchasing a home.

For a middle-income family earning approximately ₹1,20,000 per month, buying may be the better option if they plan to stay in the same area for several years. Homeownership provides stability, predictable housing costs, and the opportunity to build equity over time.

High-income buyers earning ₹3,00,000 or more per month often have greater financial flexibility. They may find it easier to afford a down payment, qualify for favorable mortgage terms, and manage maintenance expenses. In many cases, purchasing a home can serve as both a lifestyle upgrade and a long-term wealth-building strategy.

Ultimately, income alone should not determine whether you rent or buy. Factors such as debt levels, savings, job stability, housing market conditions, and future plans are equally important. Evaluating your complete financial picture can help you choose the option that best supports your long-term goals.

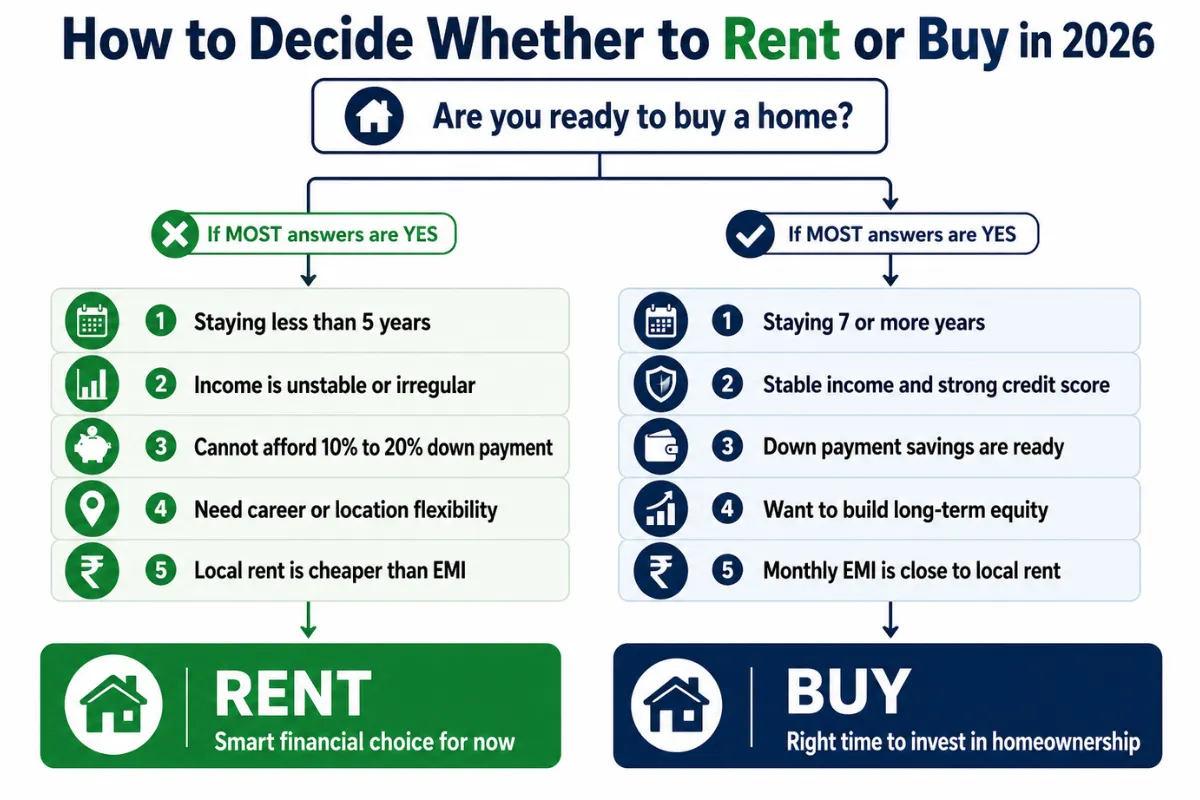

How to Decide Whether to Rent or Buy

Choosing whether to rent or buy depends on your budget, long-term goals, lifestyle, and financial readiness. Before making a decision, review this rental agreement and legal checklist to understand important terms, responsibilities, and legal considerations that can affect your housing choice.

Decision Checklist

The rent-versus-buy decision is ultimately personal. Market conditions matter, but your financial situation, lifestyle preferences, and long-term plans matter even more. Before making a commitment, take time to evaluate the factors that will have the biggest impact on your finances.

Ask yourself:

- Will I stay in the same location for at least 7 years?

- Can I comfortably handle maintenance and repair costs?

- Do I have enough emergency savings before buying a home?

- Would investing the down payment and monthly savings generate better returns?

- Do I value flexibility and mobility?

Answering these questions honestly can provide more clarity than any market forecast. Buying may look attractive on paper, but if ownership creates financial stress, renting could leave you with greater flexibility and more opportunities to build wealth through investing.

On the other hand, if you have stable finances, long-term housing plans, and the ability to manage ownership costs, buying can become a powerful wealth-building tool.

There is no universal right answer. The best choice is the one that aligns with your financial goals, risk tolerance, and lifestyle priorities – not simply what others are doing.

Frequently Asked Questions

Is it cheaper to rent or buy a home in 2026?

The answer depends on your location, mortgage rate, down payment, and expected length of stay. In many markets, renting offers lower monthly costs, while buying can become more cost-effective over the long term through equity growth and property appreciation.

How many years should I stay in a home for buying to be a smart financial decision?

Most financial analyses suggest that buying becomes more attractive when you plan to stay in a property for at least 7–10 years. A longer ownership period helps offset upfront costs such as down payments, closing fees, and moving expenses.

Does renting mean losing money compared to buying?

Not necessarily. Renting can provide greater flexibility, lower upfront costs, and the ability to invest savings elsewhere. In some situations, investing the difference between renting and buying can generate significant long-term returns.

How many years should I stay in a home for buying to be a smart financial decision?

Many buyers underestimate ongoing expenses such as maintenance, repairs, property taxes, insurance, and opportunity costs. These costs can significantly affect the true affordability of owning a home.

Should I buy a home if mortgage rates remain above 6%?

Higher mortgage rates increase borrowing costs, but buying may still make sense if you have stable finances, plan to stay long term, and can comfortably cover the monthly housing costs. The decision should be based on your overall financial situation rather than interest rates alone.

Conclusion

The rent-versus-buy decision in 2026 is less about following conventional wisdom and more about understanding your financial reality. Renting can provide flexibility, stronger cash flow, and investment opportunities, while buying offers long-term stability and the potential to build equity. The option that saves you more money depends on factors such as your time horizon, local housing market, mortgage rates, and personal goals. Rather than asking whether renting or buying is universally better, ask which choice best supports your lifestyle and financial future. The smartest decision is the one that aligns with both your budget and long-term objectives.